Your community is the key to financial freedom

ChipJar helps your community pool funds, lend to each other and build financial resiliency – all in one app.

Start a jarThe American problem…

in an emergency

emergency with additional credit access

extractive interst rate

…for most it's hard to access funds at a fair price

Not a bank. Not a payday lender.

Your own financial community,

on your own rules.

Explore how just one choice can build a strong financial base — or a spiral of loans that are hard to escape…

How it works

Not a one-time payout. A revolving mutual aid engine where your community’s safety net builds with every cycle.

Start a jar

Invite people you trust. Set contribution amount and schedule together.

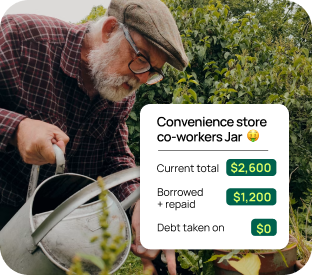

Build the fund

Everyone chips in regularly. The Jar grows as a collective safety net.

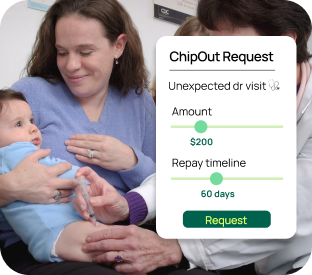

Chip out

Request a Chip. Group approves on their terms — amount, fee, timeline.

Grow together

Chips repaid, Jar recharges. The fund deepens. The community compounds.

Who it’s for

Built for communities that

build each other up

Family

Formalize the support you already give each other. Build generational savings along the way.

Friends

Your group chat already covers each other. A Jar makes it trackable, fair, and accountable.

Colleagues

Coworkers, unit members, shift teams — built-in accountability with people you see every day.

Communities

Churches, neighborhoods, cultural groups — any community with trust and shared goals.

How ChipJar compares

Transmission apps move money. Banks lend it. ChipJar builds community wealth.

| Feature | ChipJar | Venmo/ |

Unsecured Bank loan | PayDay Lender |

|---|---|---|---|---|

| Captial stays among members | ✓ | ✓ | ✕ | ✕ |

| No credit check | ✓ | ✓ | ✕ | ✓ |

| Jar-set terms | ✓ | ✕ | ✕ | ✕ |

| Invite-only with trusted community | ✓ | N/A | N/A | N/A |

| Priced to build resiliency | ✓ | N/A | ✕ | ✕ |

See how much you’d save

Stop renting money, start owning the solution.

Cost to borrow over 60 days — across the real options

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

membership during loan

vs. the cheapest alternative alone

Frequently asked

Everything you need to know about Jars, Chips, and keeping your money safe.

What exactly is a “Jar”?

A Jar is an invite-only community fund. Members contribute on a schedule they choose, and the pooled money stays in the group. When someone needs funds, they request a “Chip” — and the group decides together whether to approve it and on what terms. Think of it as a digital version of savings circles with real financial infrastructure.

A Jar is an invite-only community fund. Members contribute on a schedule they choose, and the pooled money stays in the group. When someone needs funds, they request a “Chip” — and the group decides together whether to approve it and on what terms. Think of it as a digital version of savings circles with real financial infrastructure.

What’s a “Chip”?

A Chip is when you draw funds from your Jar. Instead of going to a bank or payday lender, you request a Chip from your community. The Jar members set the amount and repayment timeline. When you repay, the money goes back into the Jar.

A Chip is when you draw funds from your Jar. Instead of going to a bank or payday lender, you request a Chip from your community. The Jar members set the amount and repayment timeline. When you repay, the money goes back into the Jar.

Is my money safe?

Yes. All funds are held in FDIC-insured accounts through our banking partners. ChipJar provides the technology layer — we never hold or manage your money directly.

Yes. All funds are held in FDIC-insured accounts through our banking partners. ChipJar provides the technology layer — we never hold or manage your money directly.

How is this different from a lending circle?

Traditional circles (ROSCAs) are a one-shot rotation. ChipJar creates a revolving fund that stays active, with formal repayment tracking, default protection, and a banking infrastructure layer.

Traditional circles (ROSCAs) are a one-shot rotation. ChipJar creates a revolving fund that stays active, with formal repayment tracking, default protection, and a banking infrastructure layer.

What if someone doesn’t repay?

Every Jar is backed by a built-in Member Protection Reserve. A small percentage of all contributions is automatically held back — so when a default happens, the reserve absorbs most of the loss and your Jar stays healthy. Members aren’t left absorbing the full hit. ChipJar also provides automated reminders, repayment tracking, and governance tools. The social bonds keep defaults rare; the reserve keeps them survivable.

Every Jar is backed by a built-in Member Protection Reserve. A small percentage of all contributions is automatically held back — so when a default happens, the reserve absorbs most of the loss and your Jar stays healthy. Members aren’t left absorbing the full hit. ChipJar also provides automated reminders, repayment tracking, and governance tools. The social bonds keep defaults rare; the reserve keeps them survivable.

Is ChipJar available yet?

We’re building and partnering with community organizations for initial launch. Drop us a message to be among the first.

We’re building and partnering with community organizations for initial launch. Drop us a message to be among the first.

Let's build something together.

Bring ChipJar to your community, explore partnerships, or just ask a question.

hello@chipjar.io →